⁉️ Did You Know ⁉️

Many retirees are in for a surprise when they discover that their Social Security benefits are taxable!

For upper-middle-income folks with a 401k/IRA/pension, this means up to 85% of those benefits could be taxed as regular income

Let me teach you more...

You worked hard for +40 years during your career, contributed to Social Security (SS) every year, and are now ready to enjoy the fruits of your labor

Most people think they are all done with taxes associated with SS...and they would be wrong!

Most people reading this post are upper middle-income folks, with some level of outside retirement savings

For your demographic

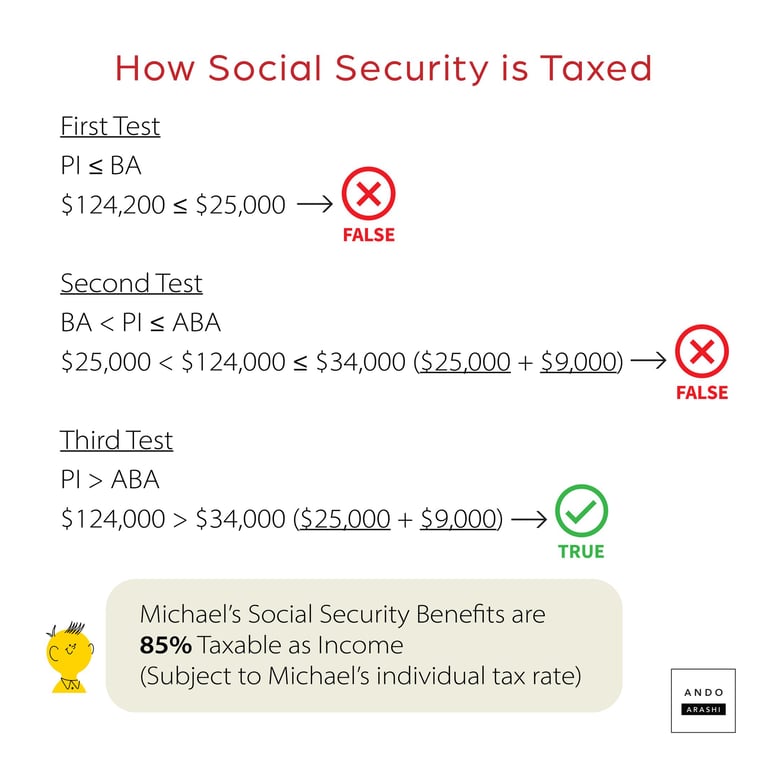

(Annual Social Security Benefits) * 85%

= Amount added to your regular income for the year, subject to your normal marginal tax rates

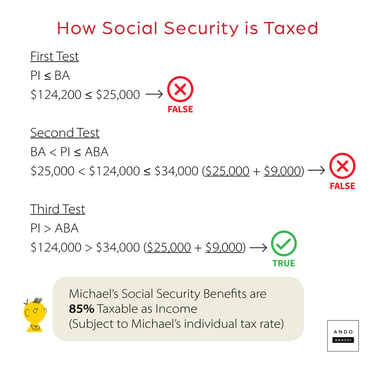

That exact taxable inclusion ratio, whether its 85%, 50% or 0% is determine by a convoluted formula

It will be made more clear by a real-life example

Let's try to explain on a basic level

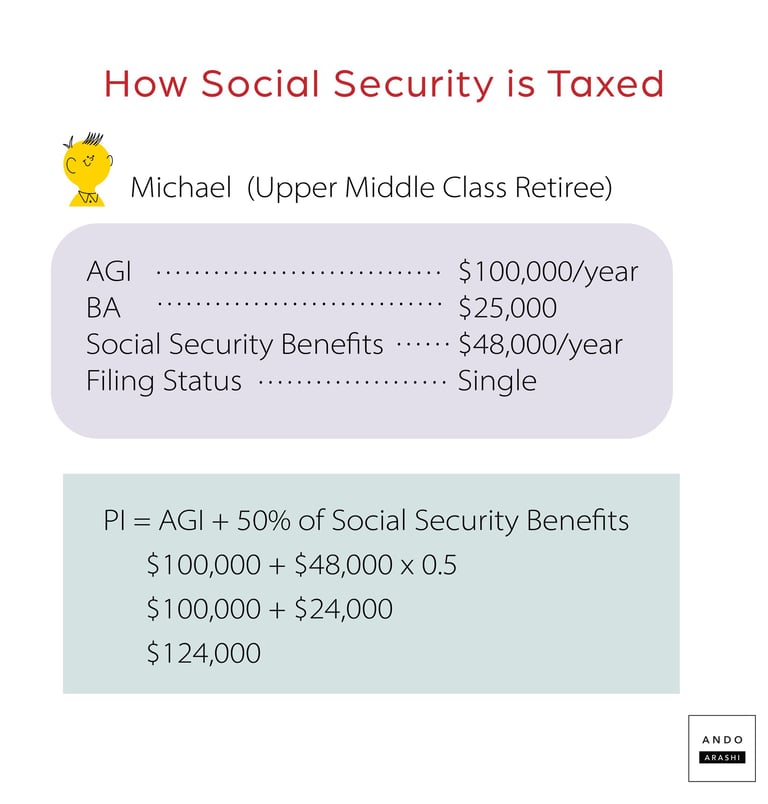

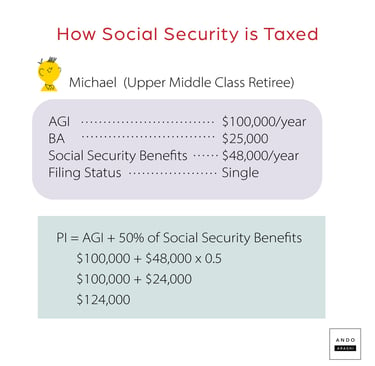

Meet Michael, an upper middle income retirew

He is a widower, and inherited his spouse's 401k and consistently saved in his own 401k for 30 years.

Bottom line, he is withdrawing roughly $100K/yr from his 401k before SS is even considered

His SS benefits are roughly $50K/yr