Japan Real Estate Tax Traps

Navigating Buying/Selling a Home in Japan

TAX

Andrew Haley

9/9/20243 min read

Congrats...You’ve achieved your dream of buying a house in Japan!

Fast forward 12 years...you sell, only to face a tax nightmare

Why are you being taxed in two countries? What’s this phantom gain thing?

Welcome to the world of foreign real estate!

Let me guide you through...

Here's a reminder how home sales are taxed inside the USA with a single homeowner named Owen

Buy Primary Home (2012) : $400K

+Renovate Home (2014): $100K

=New Adjusted Basis: $500K

Sell Primary Home (2024): $900K

-Adjusted Basis: $500K

=Realized Capital Gain $400K

Furthermore, Owen qualifies for an IRS Sec 121 Exclusion on the gain of the sale

$500K Exclusion (Married)

$250K Exclusion (Single)

Owen is single

$400K Realized Gain

-$250K Exclusion

=$150K Recognized Capital Gain

$150K *15% = $22.5K Capital Gains Tax

That is pretty basic, and most people are aware of how real estate is taxed in the USA

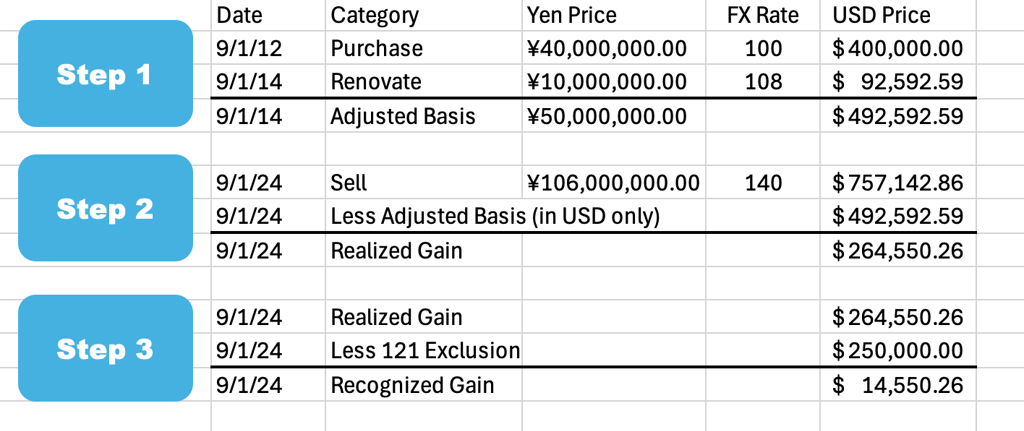

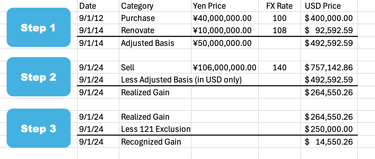

But what all facts remained the same, but property was located in Yokohama Japan?

Then Owen must consider

FX rate

Mortgage Balance

Japanese Cap Gains

FX Rate:

Owen must record the FX rate (¥-->$)

at time of purchase (2012)

at time of major renovation (2014)

at time of sale (2024)

Mortgage Balance:

Owen must track

Original Mortgage Balance (2012); both in ¥ and converted back to $

Every Monthly Payment applied to Principal; both in ¥ and converted back to $

Final Mortgage Balance (2024); both in ¥ and converted back to $

This is giant pain in the a$$

Japanese Capital Gains

As a long-term resident of Japan, Owen has also become a tax resident of Japan, and must file an annual Japanese income tax form

As such, Japan takes first position over the USA for taxing capital gains from sale of a primary residence

Japan also has a primary home exclusion and a special long-term capital gains rate for sales past 10 years

I will spare you the exact math

Essentially:

Owen had a realized capital gain ¥56M ($400K USD) --> Japanese capital gain tax ¥3.6M ($26K USD)

There is no way around this

Then USA takes 2nd position

The US answer is complex because each step in the process needs to be converted into USD

In this case, wild FX swings over a decade reduced his realized gain down to $264K

Minus $250K exclusion, Owen has recognized $14K in capital gains

Summary:

Owen paid $26K USD Capital Gains tax to Japan

Owen paid $2.1K USD Capital Gains tax to USA (multiply $14K recognized gain * 15% rate)

This double taxation could be mitigated via some of the international tax provisions on Owen's US Federal Income Tax Form

If that part wasn't complicated enough due to the currency swings...

Next there's an even more insidious calculation

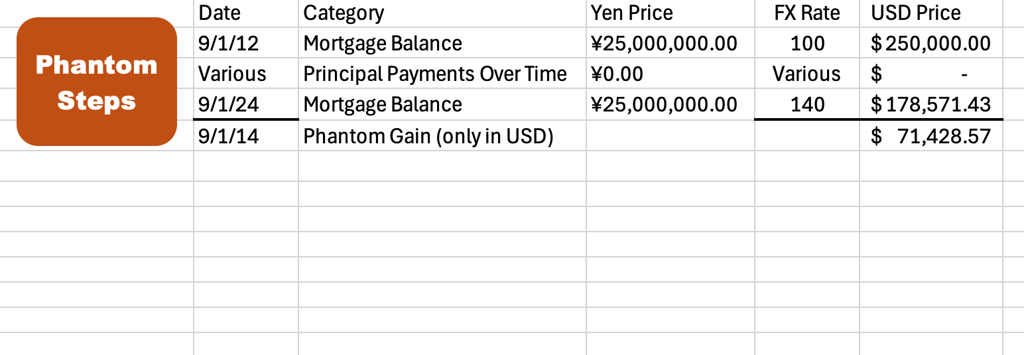

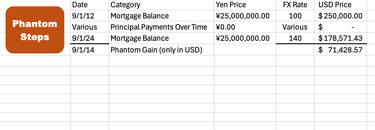

Phantom Gain (IRS Sec 988)

= Mortgage Value Fluctuations from FX swings

Debt value ⬆️ in USD = No Deduction

Debt value ⬇️ in USD = Ordinary Income

Our first calculation was for the regular capital gain tax; next is for phantom gain because the Yen declined by 40% while owner had this mortgage

In this case, we keep it simple and assume the owner started with a $250K Japanese mortgage and somehow never had to pay it down

At time of sale, Owen has $71K phantom gain which will be considered ordinary income in the USA

In real life, you would also have to track each monthly principal payment and associated FX rate on that day to arrive at the correct phantom number

So the phantom gain is quite cunning...after all Owen personally didn't cause a weaker Yen!

And Owen’s life is now in Japan, conducted mostly in Yen, so he didn't really benefit from that currency weakness either

But what can I tell you?

Those are the rules!

And if the FX rate had gone the other way (getting stronger), then there is generally no allowed deduction (unless you are in some kind of disaster area).

Also seems quite insidious

Come on IRS!

Help out the common Expat here!

And if the FX rate had gone the other way (getting stronger), then there is generally no allowed deduction (unless you are in some kind of disaster area).

Also seems quite insidious

Come on IRS!

Help out the common Expat here!

Other considerations with foreign real estate

Inheriting property: Step Up Basis still applies (with associated FX conversions)

1031 Exchange: Only works foreign --> foreign property, can't mix with domestic

FBAR reporting triggered if property gains deposited in local bank

So that's an overview of buying/selling foreign real estate.

Have you ever purchased and sold a property in Asia before?

What was your experience?

I'd love to hear more about it!

Ando Arashi

878-223-0083

hello@ando-arashi.com

Ando Arashi® is a registered trademark of Ando Arashi LLC.

The firm is a registered investment adviser with the state of Pennsylvania, and notice-filed in Texas and may only transact business with residents of those states, or residents of other states where otherwise legally permitted subject to exemption or exclusion from registration requirements. Registration with the United States Securities and Exchange Commission or any state securities authority does not imply a certain level of skill or training.

© 2026 Ando Arashi LLC. All rights reserved.